Running a grooming salon means juggling sharp tools, stressed animals, and client expectations every single day. What most salon owners don't realize until it's too late is that their insurance coverage has massive gaps — gaps that only show up when something goes wrong.

A grooming salon in Ohio got hit with a $47,000 lawsuit after a dog jumped off the table and fractured its leg. Their general liability covered $15,000. The owner paid the rest out of pocket, then closed the business three months later. The worst part — they'd been paying for insurance for eight years thinking they were fully protected.

This isn't about scaring you into buying more insurance. It's about building a practical system that actually protects your business while keeping costs reasonable. The pattern across grooming operations is clear: salons that dodge expensive disasters don't just buy policies — they build operational systems around their coverage.

Why Standard Pet Groomer Insurance Packages Leave You Exposed

Walk into any insurance broker's office and mention you run a grooming salon. They'll pull out their "pet business package" — usually general liability, maybe some property coverage, and call it done. These packages work fine for pet stores. For grooming salons, they miss a huge chunk of your actual risk exposure.

-

Sharp equipment near moving animals

-

Chemical products that can cause reactions

-

Animals with unknown behavioral triggers

-

Physical lifting that leads to worker injuries

-

Valuable client property (expensive breeds)

-

Equipment worth $15,000–$40,000

A typical grooming salon faces liability from at least a dozen different angles. Most only have coverage for three or four. The gaps aren't obvious until an incident happens, and by then you're writing checks your business can't cash.

What actually matters is matching your coverage to your specific operational risks, documenting everything properly, and maintaining a compliance rhythm that catches problems before they get expensive.

The Core Coverage Framework Every Salon Actually Needs

General Liability (The Foundation)

Never miss a grooming appointment again.

Furlyly helps you book, confirm, and manage every pet grooming appointment effortlessly.

- Unified appointment scheduling

- Automated client reminders

- Staff availability & shift management

No credit card required

This covers the obvious stuff — dog bites another dog, client slips in your lobby, groomer accidentally cuts a pet. Most salons have this. The problem is they usually carry the wrong limits.

Minimum coverage should be $1 million per occurrence, $2 million aggregate. Anything less and one serious bite incident wipes you out. But here's what brokers rarely mention: the per-incident deductible matters more than the total coverage amount. A $5,000 deductible on a $1 million policy means you're absorbing the first $5,000 of every single claim. For a small salon doing around $200,000 annually, three minor incidents in a year could mean $15,000 out of pocket.

Better approach: pay slightly higher premiums with a $500–$1,000 deductible. You'll spend an extra $40–$70 per month but save thousands when incidents happen.

Professional Liability (The Grooming-Specific Shield)

General liability doesn't cover "professional services" claims. If you nick a show dog before a competition, or a dog has an allergic reaction to your shampoo, that falls into professional liability territory. A significant portion of grooming salons don't have this coverage at all.

A groomer in Phoenix trimmed a Poodle's coat too short before a show. The owner claimed $8,000 in lost prize money and breeding fees. General liability denied it. Professional liability would have covered it.

| Coverage | Recommended Limits/Notes |

|---|---|

| General Liability | Minimum $1 million per occurrence, $2 million aggregate; prefer $500–$1,000 deductible |

| Professional Liability | Coverage sweet spot: $500,000 per incident, $1 million aggregate. Costs roughly $600–$900 annually for a three-person salon. |

| Business Property | Cover computer systems with client data; Inventory; Improvements to leased spaces; Business interruption costs. Understand replacement cost vs actual cash value. |

| Workers' Compensation | Workers' comp for groomers runs about $2.50–$4.00 per $100 of payroll. |

| Commercial Auto | Personal auto insurance void for business use; mobile groomers need commercial auto; coverage follows business use. |

Business Property (Beyond Just Equipment)

Most groomers insure their tables and dryers. Smart ones also cover:

-

Computer systems with client data

-

Inventory (shampoos, retail products)

-

Improvements to leased spaces

-

Business interruption costs

The trick with property coverage is understanding replacement cost versus actual cash value. A $3,000 hydraulic table might only be worth $800 after depreciation. When it breaks, actual cash value gives you $800. Replacement cost gives you $3,000 toward a new one. That difference matters more than most owners realize until they're shopping for equipment after a loss.

Workers' Compensation (Even for "Independent Contractors")

States are cracking down on groomer classification. California, New York, and Massachusetts already require workers' comp for most grooming arrangements. Even if your groomers are 1099 contractors, if they get hurt and you don't have coverage, you're personally liable.

Workers' comp for groomers runs about $2.50–$4.00 per $100 of payroll. For a groomer making $40,000, that's $1,000–$1,600 annually. Skip it and a back injury could cost you $80,000 in medical bills and lost wages.

Commercial Auto (The Mobile Grooming Must-Have)

Personal auto insurance becomes void the second you use your vehicle for business purposes. One accident on the way to a client's house and you're effectively uninsured. Mobile groomers need commercial auto coverage, full stop.

But even salon-only operations need this if employees ever drive for business — bank deposits, supply runs, dropping a dog at the vet. The coverage follows the business use, not who owns the vehicle.

Building Your Risk Documentation System

Incident Report Templates

Create three separate templates:

Type A: Client Property Damage

-

Exact time and date

-

Which groomer was handling the pet

-

Detailed description of what occurred

-

Photos from multiple angles

-

Client notification timestamp

-

Witness names and statements

Type B: Injury (Human or Animal)

-

Injured party details

-

Exact location in salon

-

Contributing factors (wet floor, equipment issue)

-

First aid provided

-

Medical attention timeline

-

Follow-up communication log

Type C: Equipment/Property Damage

-

Equipment identification (model, serial number)

-

Last maintenance date

-

Damage description

-

Operational impact

-

Temporary solutions implemented

-

Repair/replacement timeline

Store these digitally with automatic date stamps. Paper versions get lost, damaged, or quietly edited after the fact. When an adjuster asks for documentation six months later, you need clean, timestamped records — not a folder of handwritten notes.

Store incident reports digitally with automatic timestamps to preserve integrity.

Certificate Tracking for Vendors and Contractors

Every vendor who enters your salon should provide a certificate of insurance. Mobile groomers renting space, delivery drivers, maintenance contractors — all of them. Without their certificates on file, their incidents can become your liability.

-

Mark expiration dates in your calendar

-

Request updates 30 days before expiration

-

Keep certificates organized by vendor type

-

Include insurance requirements in all vendor contracts

One HVAC contractor without proper coverage drops a unit through your roof — suddenly you're filing the claim and eating the deductible.

Lease and Contract Clause Alignment

Your lease probably has insurance requirements buried on page 12. Your insurance policy has exclusions buried on page 47. When these don't align, you're exposed.

-

Lease requires $2 million liability, you have $1 million

-

Policy excludes "damage to rented premises," lease makes you liable for it

-

Lease requires naming landlord as additional insured, you never added them

Review both documents quarterly. Leases get amended, policies get renewed, terms change. Missing one update could void coverage at the worst possible moment.

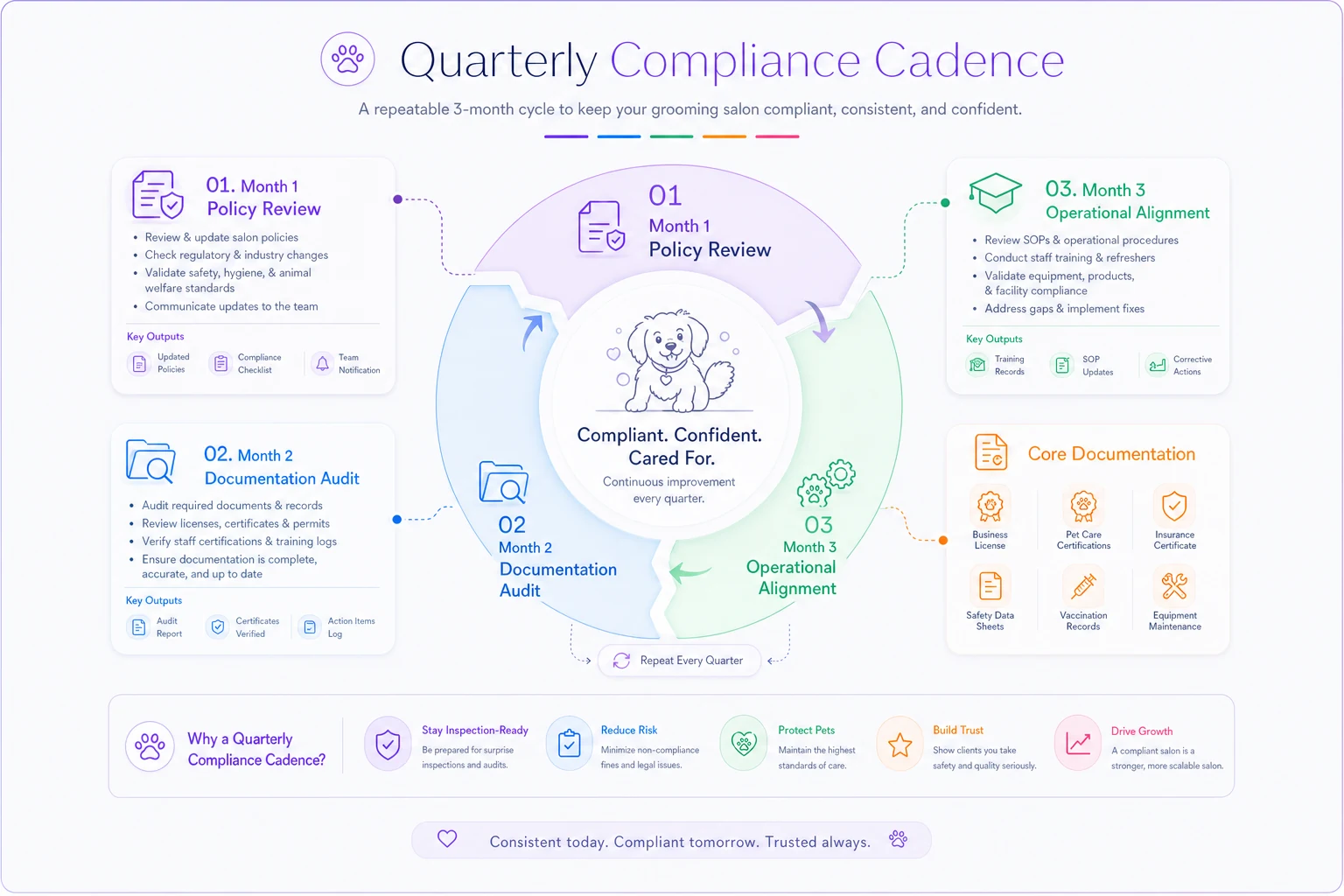

The Quarterly Compliance Cadence That Actually Gets Done

Maintaining a solid pet groomer insurance checklist isn't about creating a perfect system once. It's about a rhythm that catches problems before they cost money.

Here's a simple workflow to visualize the quarterly cadence.

Month 1 of Each Quarter: Policy Review

-

Verify all policies are current

-

Check coverage limits against actual revenue

-

Review recent claims for patterns

-

Update property values if equipment changed

-

Confirm all locations are covered (if operating multiple sites)

Month 2 of Each Quarter: Documentation Audit

-

Review all incident reports from the past quarter

-

Update emergency contact information

-

Check vendor certificates for upcoming expirations

-

Verify employee files have current information

-

Test backup systems for digital records

Month 3 of Each Quarter: Operational Alignment

-

Walk through the salon and note any new risks

-

Update safety protocols based on incidents

-

Review client waivers and intake forms

-

Check equipment maintenance schedules

-

Run a quick safety training refresher with staff

This whole cadence takes maybe 3–4 hours per quarter. Compare that to the 40+ hours you'll spend managing one uncovered claim.

Real Warning Signs Your Coverage Has Dangerous Gaps

These patterns usually indicate insurance problems are already brewing:

Revenue growing but coverage static: If revenue jumped 30% but limits haven't changed in two years, you're underinsured. Claims get calculated against current operations, not what the business looked like when you bought the policy.

New services without policy updates: Added doggy daycare? Started selling CBD products? Offering shuttle service? Each new offering adds risk categories your original policy might not touch.

Incident patterns without root cause fixes: Three slip-and-falls in six months? Four aggressive dog incidents in a quarter? Your insurer will either drop you or spike your premiums at renewal. Better to actually fix the problem — improve your flooring, add safety protocols for aggressive pets, tighten your intake process.

Deductibles eating into cash flow: Paying deductibles more than twice a year means either your deductible is too low or your operations need real safety attention.

Vendor incidents becoming your problem: Delivery driver damages a client's car in your lot. Mobile groomer injures a dog while renting your space. If you're absorbing these claims, your vendor insurance requirements are too loose.

The Hidden Costs of Being Underinsured

The obvious cost is paying claims out of pocket. The less obvious costs tend to hurt longer:

Credit destruction: A $30,000 judgment you can't pay immediately hits your business credit. Try financing new equipment or signing a lease after that.

Stress bleeding into operations: Owners dealing with active lawsuits make poor operational decisions. Quality drops, staff leave, clients notice.

Reputation damage: Even when you win, the story spreads. "I heard they had some legal trouble" is enough to lose prospective clients who don't know the details.

Growth paralysis: You can't sign a lease for a second location without proper coverage in place. Can't get certain vendor accounts. Can't attract experienced groomers who want stability.

A salon in Denver skimped on insurance to save around $200 a month. One dog fight led to a $65,000 judgment. They paid it down over three years but couldn't finance new equipment, lost their best groomer to a competitor, and eventually sold the business for well below its potential value.

Converting Insurance from Cost Center to Operational Asset

Smart salons don't just buy insurance — they build operations around their coverage structure.

Turn requirements into selling points: "Fully insured and bonded" means nothing to most clients. "We carry $2 million in coverage specifically for pet injuries" tells nervous owners you're serious about safety and accountability.

Use documentation for training: Those incident reports are actually useful training materials. Real situations from your own salon teach better than generic safety videos from some national provider.

Let coverage guide service decisions: Thinking about adding mobile grooming or daycare? Check insurance costs first. If coverage triples your overhead, maybe the service doesn't pencil out.

Build vendor partnerships on insurance alignment: Vendors with solid coverage become preferred partners. Those without it get replaced. This naturally improves overall operational quality over time.

Where Operational Software Fits Into This

The quarterly compliance cadence works, but tracking everything manually means something always slips. Certificate expirations sneak up. Incident reports get filed inconsistently. Documentation exists somewhere but nobody can find it when the adjuster calls.

Operational software with built-in automation changes that dynamic. Instead of manually remembering to check vendor certificates, the system flags them 30 days before expiration. Incident reports follow the same template every time with automatic timestamps. All documentation lives in one searchable place instead of across three folders and two email threads.

The more useful benefit is pattern recognition. Platforms that log every incident can surface trends you'd otherwise miss — like Wednesday afternoons having significantly more incidents, or one groomer accounting for a disproportionate share of equipment damage. Those insights let you fix problems before your insurance company notices them at renewal.

More sophisticated platforms can also match operations to insurance requirements automatically. Lease requires specific coverage levels? The system flags when you're running below limits. Policy excludes certain service types? The system surfaces that before you add them to your menu.

The point isn't to automate judgment — it's to make compliance automatic so it doesn't depend on someone remembering. When documentation and tracking handle themselves, maintaining proper coverage becomes part of normal operations instead of a quarterly scramble.

The Quarterly Review That Actually Protects Your Business

Insurance isn't about paranoia or throwing money at premiums. It's about understanding what risks your salon actually faces, covering them appropriately, and running operations that reduce claims in the first place.

Salons that survive long-term don't necessarily carry the most insurance — they carry the right insurance alongside solid operational systems. They document everything, track compliance consistently, and fix problems before they turn into claims.

Your pet groomer insurance checklist isn't a one-time setup. It's a living system that needs quarterly attention and honest operational alignment. Get it right and insurance becomes a competitive advantage. Ignore it and you're one bad afternoon away from losing everything you've spent years building.

The difference between salons that close after a major incident and those that recover is usually a few hours of quarterly compliance work and systems that support it. For a business you've put real time and money into, that's a reasonable investment.

Ready to streamline your grooming business?

Join 500+ pet groomers using Furlyly to save time, reduce scheduling conflicts, and deliver exceptional client experiences.